Stablecoin treasury architecture fails when teams treat liquidity like a wallet balance

Why serious stablecoin treasury systems need explicit rules for custody, liquidity, governance, issuer choice, reconciliation, and yield rather than treating stablecoin balances as simple digital cash.

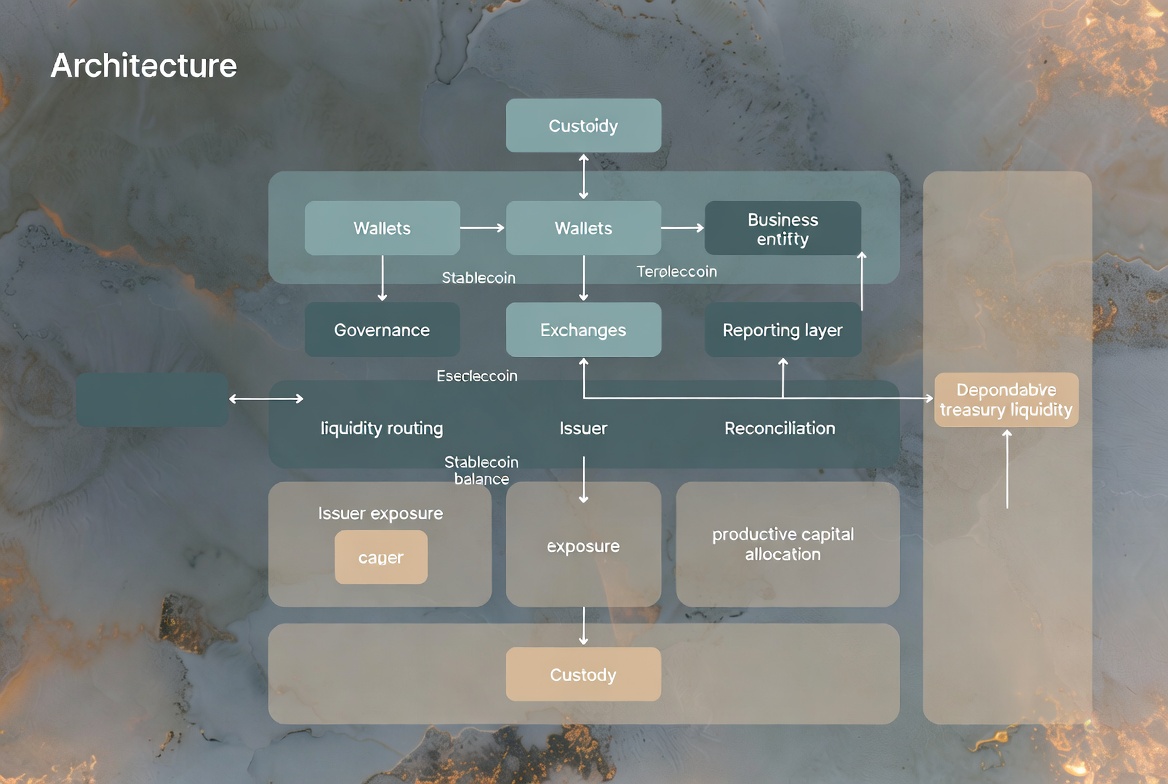

Stablecoins are often introduced to treasury teams as if they were just faster dollars. Settlement is quicker, transfers are global, the rails are always on, and the balances are programmable. All of that is true enough to be useful, but it can also be misleading. Once stablecoins move from experimentation into real treasury operations, the problem stops being whether the asset is convenient. The problem becomes whether the organization has an architecture capable of treating digital liquidity with the same seriousness it applies to any other balance-sheet-critical resource.

That is where many treasury designs become fragile. Teams see a wallet balance and assume they are seeing liquidity. In reality, treasury liquidity is never just a number. It is a combination of custody quality, issuer risk, redemption pathways, access policy, reconciliation discipline, counterparty dependencies, movement constraints, and the operational confidence that funds can be positioned when the business actually needs them.

Stablecoin balances are not the same thing as treasury liquidity

A wallet showing a stablecoin balance can create a false sense of simplicity. The number is visible, settlement may be fast, and movement can feel immediate. But treasury liquidity is defined not only by possession. It is defined by usability under real conditions.

Can the balance be redeemed when needed. Through which counterparties. Under what limits, cutoffs, jurisdictions, and compliance checks. How concentrated is the exposure to one issuer, one venue, one chain, or one custody model. What happens if a partner becomes unavailable during a critical movement window. A balance can look liquid on-chain while being operationally brittle in exactly the moments treasury discipline is supposed to matter.

This is why stablecoin architecture should begin by separating visible balances from dependable liquidity. A serious treasury does not only ask how much it holds. It asks how much it can move, where, under what conditions, with what confidence, and how quickly that movement can be verified and reconciled.

Custody is the first architecture decision, not an implementation detail

Many teams begin stablecoin programs by choosing a wallet provider or custody partner and then treating the rest of the system as a layer on top. That sequence gets the priorities backward. Custody is not a supporting detail. It is one of the primary architecture choices because it determines how authority, safety, recovery, and treasury operations will actually work.

A treasury system has to answer practical questions before it deserves real balances. Who can authorize movement. How are approvals split. How are emergency actions handled. How are keys rotated, recovered, and monitored. What happens if one signer, one device, one provider, or one region becomes unavailable. How much of the workflow depends on one external platform staying healthy and cooperative at the same time.

This matters especially because stablecoin treasury operations often begin with an assumption of simplicity and then grow into cross-border movement, entity-to-entity transfers, vendor payouts, or capital staging across venues. Once that happens, custody quality becomes inseparable from operating confidence. A weak custody model can turn fast assets into slow decisions.

Issuer choice is a treasury policy question

Stablecoins are often grouped together as if the main difference were ticker symbol. That is too casual for treasury architecture. Issuer choice changes the risk profile of the whole system.

Different issuers bring different reserve models, redemption practices, compliance relationships, geographic exposure, operational reputation, and ecosystem fit. Even if two assets are both dollar-pegged, they may not behave the same way when the treasury team needs to move size, exit a position, change chains, respond to partner concerns, or satisfy internal policy constraints. Treating stablecoin selection as a convenience decision is one of the easiest ways to import hidden risk into the treasury stack.

A mature architecture therefore treats issuer exposure as a governed dimension of liquidity, not as a default. The right question is not only which stablecoin is easiest to use today. It is which combination of issuers, partners, and rails preserves operational choice without creating fragile concentration.

Treasury governance has to exist before yield does

One of the fastest ways to weaken a stablecoin treasury program is to start chasing productive use before governance is mature enough to control it. The asset may be stable, but the workflows around it can become unstable very quickly once teams add yield routes, DeFi positions, lending exposure, cross-chain movement, or automated capital allocation.

Governance is what decides which uses are permitted, what exposure levels are acceptable, who approves exceptions, how counterparties are reviewed, how strategy changes are recorded, and how the organization distinguishes liquidity capital from productive capital. Without that structure, treasury stops being policy-driven and starts becoming opportunistic.

This is why productive treasury design should be layered. Custody, governance, liquidity, and yield are connected, but they should not be treated as if they become safe at the same time. A treasury that seeks return before it can reliably control movement, authority, and reconciliation is not optimizing. It is just reaching further than its architecture can support.

Reconciliation is where programmable money stops feeling magical

Stablecoin treasury products are often sold on speed and programmability, which are real advantages. But those strengths can distract teams from the least glamorous requirement in the system: reconciliation.

As soon as stablecoins interact with internal ledgers, ERP processes, treasury management workflows, reporting obligations, audit controls, or multi-entity accounting, the architecture has to explain how token movement becomes financial truth inside the company. Which transaction maps to which business event. Which wallet belongs to which entity. Which movement was operational, internal, client-facing, or strategic. Which balances are liquid, restricted, pending, or already committed elsewhere.

Without strong reconciliation, stablecoin operations create a dangerous illusion of clarity. The chain shows movement, but the business does not yet know what the movement means. In treasury, that gap is unacceptable. Fast settlement is only useful when it leads to fast, defensible understanding.

Cross-border and always-on liquidity are operational advantages only if controls keep up

One of the strongest stablecoin use cases is the ability to move value across borders and across time zones without waiting for banking windows or correspondent chains. That can meaningfully improve capital efficiency and reduce liquidity latency. But operational advantage only becomes durable when the control model evolves with it.

If treasury teams can move faster but approval design still assumes office hours, if payments can settle continuously but monitoring only works in business time, or if multi-region movement becomes easy while policy enforcement remains fragmented, then the architecture creates speed without confidence. In that state, stablecoins may reduce settlement friction while increasing governance friction.

A stronger system treats always-on liquidity as a design challenge, not only a convenience feature. It extends authorization, monitoring, issuer policy, asset allowlists, venue choices, and fraud controls into the same round-the-clock reality as the rails themselves. Otherwise the technology becomes more continuous than the organization managing it.

Productive capital and operational capital should not be modeled the same way

A treasury that uses stablecoins only as movement rails has one kind of problem. A treasury that also uses them for yield, collateral staging, DeFi access, or strategic allocation has another. One of the most important architecture decisions is refusing to model those balances as if they were interchangeable.

Operational capital exists to be available. Productive capital exists to generate return under controlled conditions. The more a treasury blurs that distinction, the more likely it is to overestimate how much safe liquidity it actually has. A balance earning yield through an external venue or protocol may still look like cash on a dashboard while carrying timing, redemption, or counterparty assumptions that make it behave very differently under stress.

This is why treasury systems need explicit categories of capital, each with its own policy, movement rules, approval paths, and reporting treatment. Not all stablecoin balances are performing the same job. Architecture has to make that visible before the organization starts believing that every tokenized dollar is equally ready for action.

Treasury architecture should preserve exit options

One of the biggest long-term mistakes in stablecoin treasury design is quietly locking the organization into one issuer, one custody stack, one settlement path, one venue network, or one operational dependency. That may feel efficient early on, but it weakens the treasury’s ability to adapt when regulations shift, partners change, costs move, or operational assumptions stop holding.

Resilient treasury architecture preserves choice. It supports more than one issuer where policy allows, more than one custody or execution path where operationally justified, and more than one route back into fiat or local rails. This is not complexity for its own sake. It is a way of preventing convenience from hardening into fragility.

Treasury does not become stronger by looking simple on a diagram. It becomes stronger by preserving the ability to reposition liquidity without redesigning the company every time a dependency changes.

Stablecoin treasury is really an infrastructure problem

The reason stablecoin treasury is becoming important is not only that the assets settle quickly. It is that they are turning liquidity into a programmable infrastructure layer for businesses that need to move capital more precisely. But infrastructure is only valuable when it is governed well.

That means custody must be explicit, issuer exposure must be deliberate, reconciliation must be tight, approvals must be modernized, productive use must sit behind policy, and liquidity must be defined by real operational access rather than by a wallet screenshot. The stablecoin itself may be simple to transfer. The treasury system around it is not.

Teams that understand this stop treating stablecoins as digital cash with better marketing. They start treating them as treasury infrastructure that needs architecture worthy of the capital it controls. That is the difference between a balance and a treasury program.

If you need help designing or hardening stablecoin treasury infrastructure (custody, governance, liquidity routing, reconciliation, yield controls, or cross-border capital movement), you can request a high-performance infrastructure engagement through the Services page or reach out directly via the Contact terminal.